US Manufacturing Expansion Accelerates in May

Stronger new orders, rising production and broad-based industry growth offset ongoing pricing pressures for US manufacturers

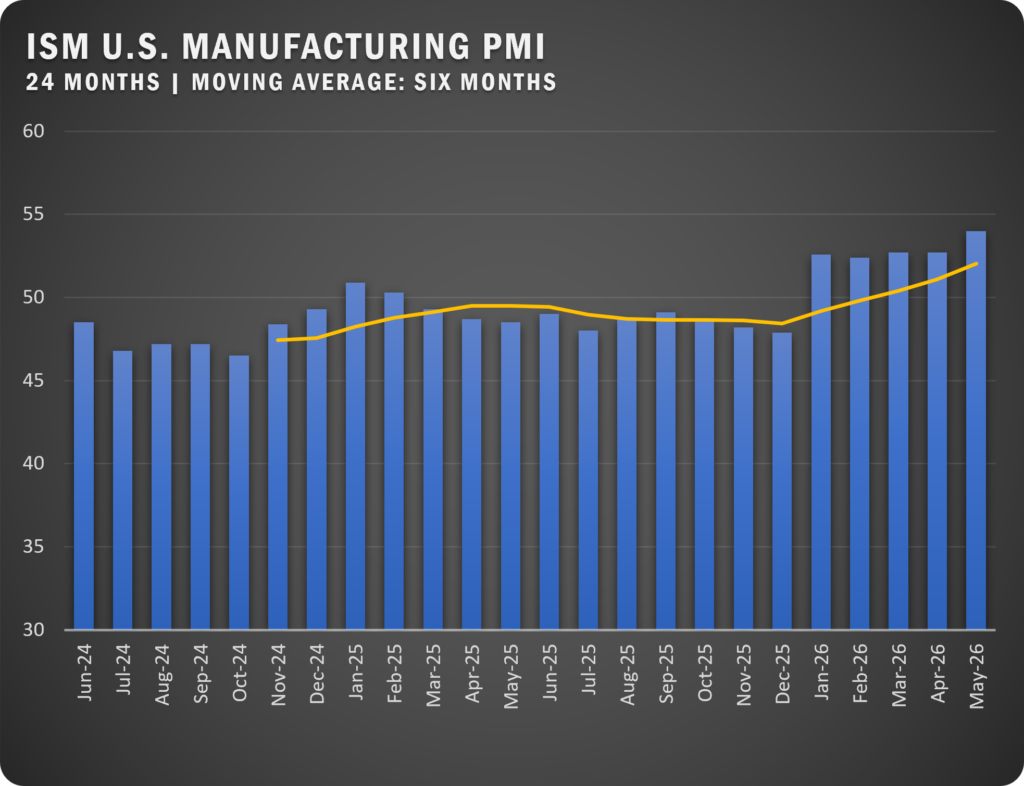

U.S. manufacturing activity expanded for the fifth consecutive month in May, according to the latest ISM® Manufacturing PMI Report. Growth accelerated during the month, supported by stronger demand, continued production gains and improving export activity, pushing the PMI to its highest level in three years.

The Manufacturing PMI registered 54.0 percent in May, up 1.3 percentage points from April and reaching its strongest reading since May 2022. The broader U.S. economy also continued to grow, extending its expansion streak to 19 consecutive months.

Demand indicators strengthened further during the month. The New Orders Index climbed to 56.8 percent, increasing 2.7 percentage points from April and marking a fifth consecutive month of expansion. Export demand also improved, with the New Export Orders Index returning to growth territory at 50.6 percent. Meanwhile, the Backlog of Orders Index increased to 52.2 percent, signaling continued pressure on manufacturing capacity.

Production remained a key driver of overall growth. The Production Index rose to 54.3 percent, its seventh consecutive month in expansion territory. Employment conditions improved as well, with the Employment Index gaining 2.2 percentage points to 48.6 percent. While hiring remained slightly below expansion levels, survey respondents were evenly split between managing headcount and actively adding workers.

Supply chain conditions remained tight. The Supplier Deliveries Index held at 60.6 percent, matching April’s reading and remaining at its highest level since May 2022, reflecting continued delivery delays. Inventories improved modestly, with the Inventories Index increasing to 49.9 percent, while the Customers’ Inventories Index remained in “too low” territory despite showing improvement. Historically, low customer inventories often support future production growth as replenishment demand increases.

Price pressures remained elevated, though they eased slightly from April’s levels. The Prices Index registered 82.1 percent, indicating continued cost inflation across the manufacturing sector. Imports expanded at a faster pace, rising to 53.0 percent as companies sought additional materials and components to support production requirements.

Looking across the manufacturing landscape, growth was widespread. Sixteen industries reported expansion in May, while only Wood Products remained in contraction. All six of the largest manufacturing industries expanded during the month, led by Computer & Electronic Products, Machinery, Transportation Equipment, Petroleum & Coal Products, Chemical Products and Food, Beverage & Tobacco Products. Only 2 percent of manufacturing GDP contracted in May, down sharply from 19 percent in April, suggesting that growth has become increasingly broad-based despite continued concerns regarding geopolitical instability, energy costs and pricing volatility.

COMMODITIES

Up in Price: Acrylic Products (2); Aluminum (30); Aluminum Products (2); Brass; Carbides; Chemical Products (3); Cooking Fats and Oils (3); Copper (11); Copper Based Products (6); Corn (3); Corrugated Products (2); Diesel Fuel (3); Electronic Components (5); Ethylene; Freight (3); Fuel (3); Gasoline; Maintenance, Repair, and Operating (MRO) Supplies; Memory Components (3); Metal Products (2); Methanol (3); Ocean Freight; Oil (2); Oil Based Products (2); Packaging Materials (2); Paper Products (2); Petroleum Based Products (2); Plastic Based Products (2); Plastics (3); Polyethylene Resins (2); Polypropylene; Resins (4); Soybean Products (3); Steel (7); Steel — Carbon (2); Steel — Hot Rolled (5); Steel — Stainless (4); Steel Products (6); Sulfur Products (2); Transportation Costs (2); Trucking Services; Tungsten Products (4); and Wire and Cable (2).

Down in Price: None.

In Short Supply: Aluminum (2); Electrical Components (11); Electronic Components (15); Memory (5); Propylene Glycol (2); Resins; Semiconductors (3); Steel Products; and Tungsten Products.

US SECTOR REPORT

ISM Growth Sectors (16): Printing & Related Support Activities; Textile Mills; Nonmetallic Mineral Products; Paper Products; Electrical Equipment, Appliances & Components; Plastics & Rubber Products; Primary Metals; Miscellaneous Manufacturing; Computer & Electronic Products; Furniture & Related Products; Machinery; Transportation Equipment; Petroleum & Coal Products; Chemical Products; Fabricated Metal Products; and Food, Beverage & Tobacco Products.

ISM Contraction Sectors (1): Wood Products.

MAY ISM REPORT COMMENTS

(U.S. Manufacturers)

Transportation Equipment: “Impact of Iran conflict starting to directly and negatively impact cost of supply chain. Oil and related commodities are escalating in price.”

Machinery: “The Middle East conflict is triggering shipment delays and uncertainties. Elevated gas prices and inflation will surely impact our purchases. However, over the last quarter, we’ve seen increased demand that was unexpected.”

Chemical Products: “Continuing trends of 15-percent sales increase in April, cost increases on a majority of raw materials, and fuel charges on many inbound and outbound deliveries. We remain cautiously optimistic that if global economic factors stabilize and the Iran conflict ends, we can continue with increased sales and maintain acceptable margins.”

Food, Beverage & Tobacco Products: “Cost of diesel is having huge impacts on our profitability. Confusion abounds around tariff refunds. We purchase many imported goods but in most cases are not the importer of record, so it is currently unclear to what we may be entitled.”

Computer & Electronic Products: “Prices continue to rise for many products — some due to increase in data center creation for electronic components, others as a result of the Iran war and reductions in availability of oil/petroleum.”

Transportation Equipment: “Supply constraints continue to propagate and are a key headwind to supporting increased aerospace and defense demand. Semiconductors, critical minerals and certain types of raw materials are illustrative examples of sales plans at risk. Corporate risk mitigation actions are underway to secure supply in the midst of constraints.”

Miscellaneous Manufacturing: “The current atmosphere is one of extreme uncertainty and concern for the future in terms of both price stability and longer-term supply continuity related to the Iran conflict and Strait of Hormuz closure. We have a lot of negotiations in process related to requested price increases, some related to oil prices and some still fallout from the 2025 tariff/geopolitical climate.”

Electrical Equipment, Appliances & Components: “Continued dynamic random-access memory (DRAM) volatility, increased gas prices and tariffs are causing long lead constraints and price hikes that customers are not willing to bear. Panic is starting within our industry.”

Fabricated Metal Products: “Business appears to be weakening — uncertainty surrounding the Iran war, rising energy prices and customers unwilling to commit to expenditures beyond a very short term.”

GLOBAL PMI NOTES

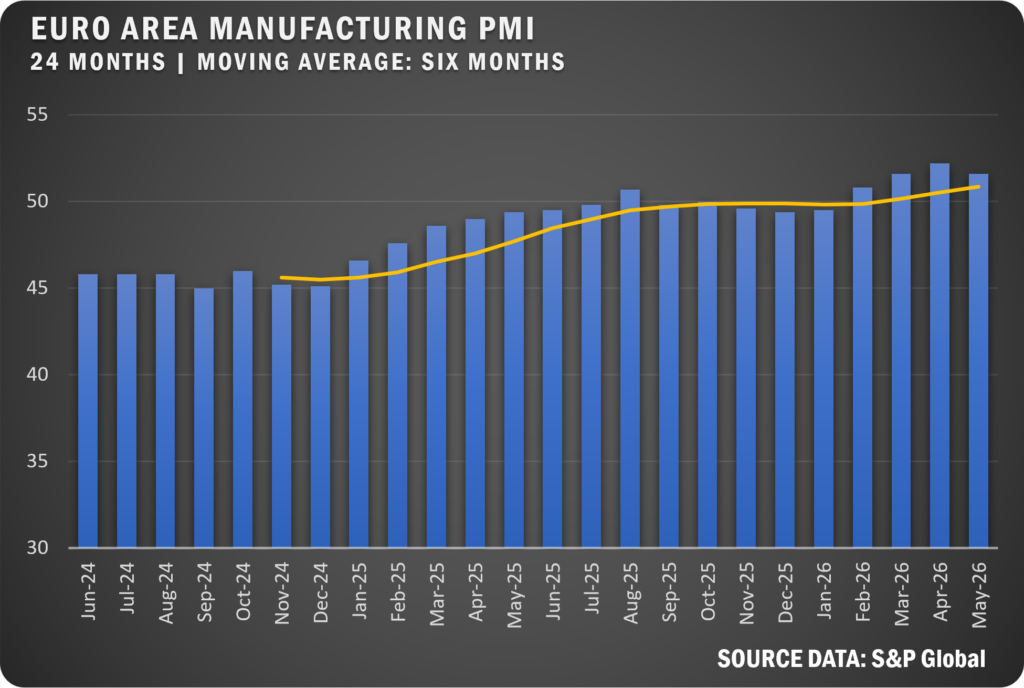

EURO AREA: Eurozone manufacturing expanded at its fastest pace since mid-2022 in March, with the PMI rising to 51.6 as output strengthened and backlogs signaled emerging capacity pressures. However, supply disruptions tied to the Middle East conflict drove up input costs sharply, while employment declined and business confidence softened.

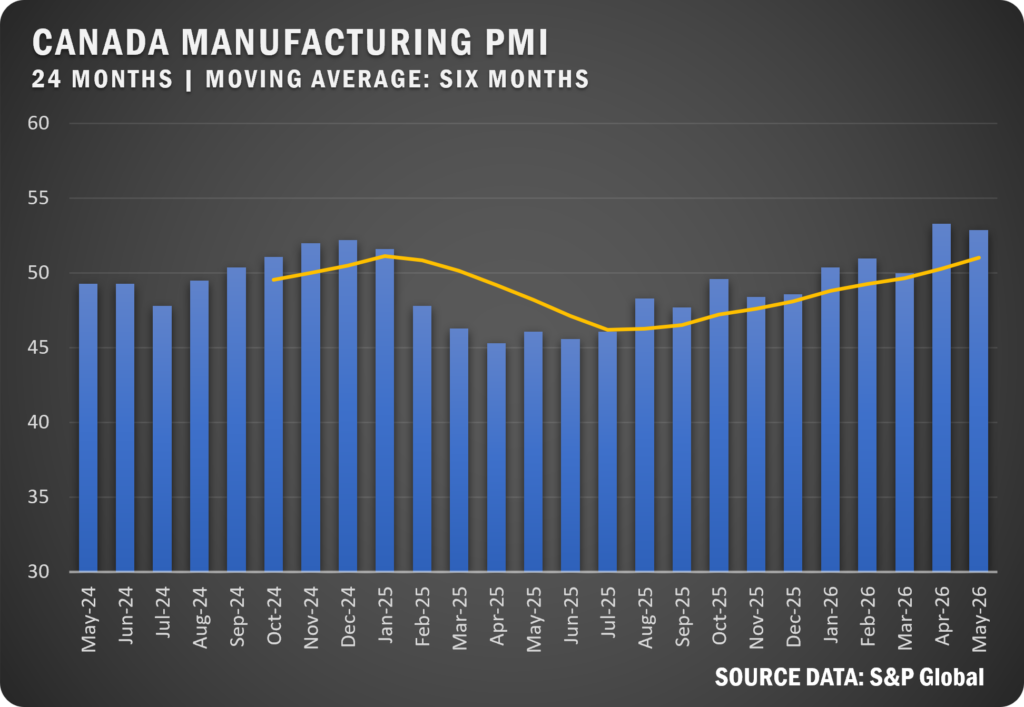

CANADA: Canada’s manufacturing sector stalled in March, with the PMI slipping to 50.0 as output contracted and new orders weakened under tariff pressures and high costs. Firms reduced staffing and faced rising input prices, while confidence fell amid geopolitical uncertainty and trade tensions.

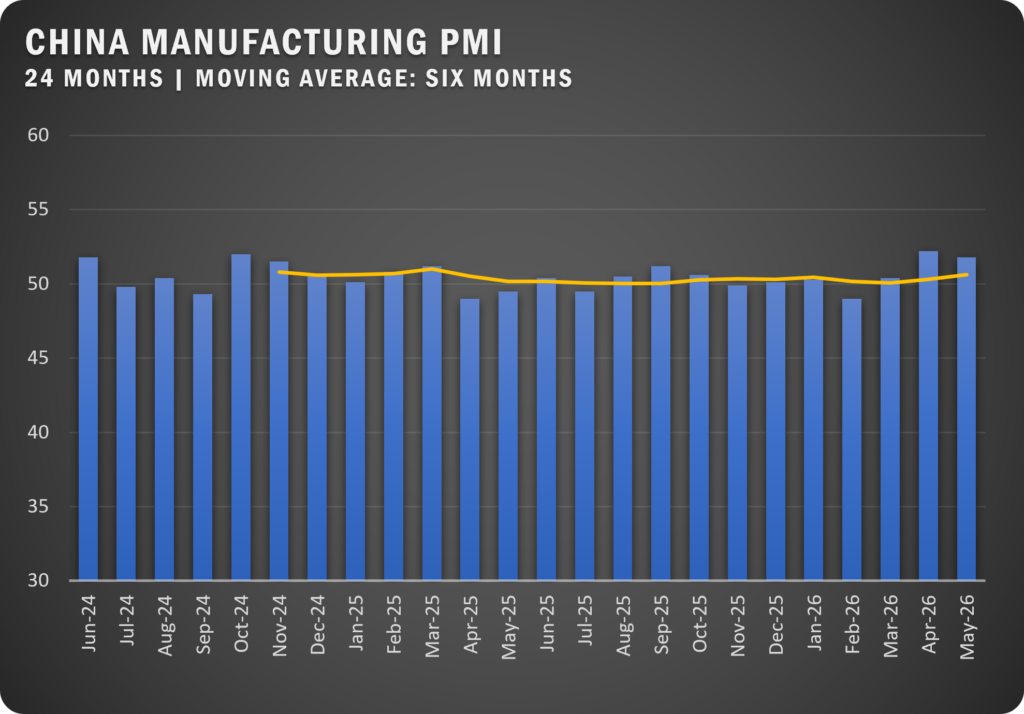

CHINA: China’s manufacturing expansion slowed in March, with the PMI easing to 50.8 as output and new orders grew at a reduced pace. Rising costs and supply delays intensified pressures, but firms remained optimistic, supported by demand, investment, and policy support.

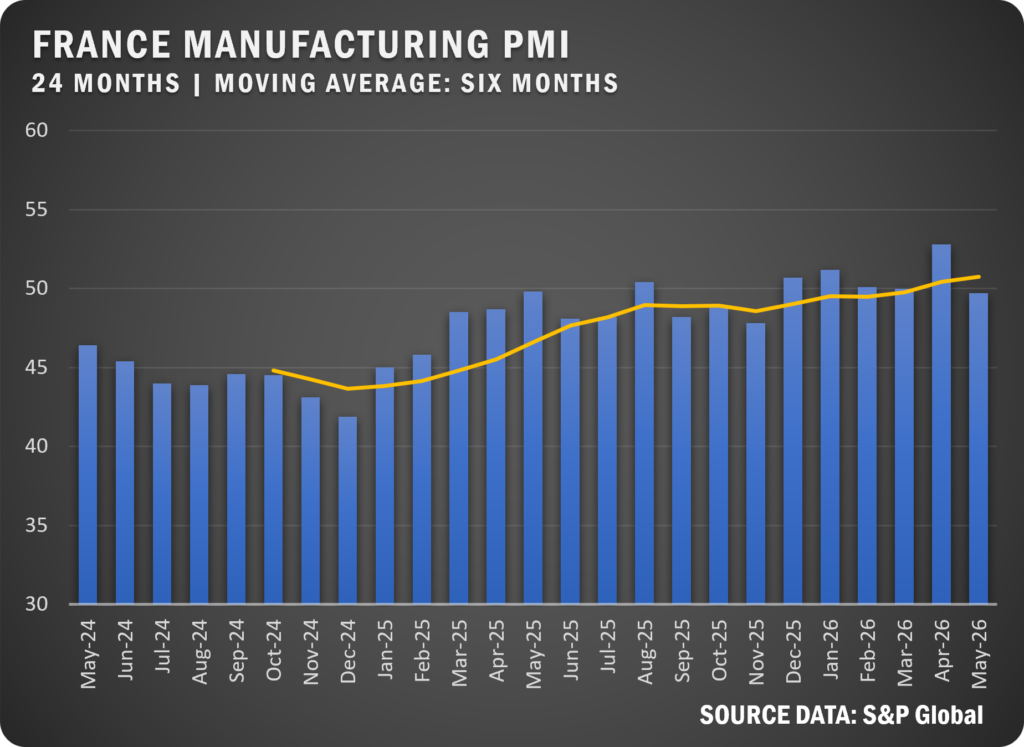

FRANCE: France’s manufacturing sector was broadly flat in March, with the PMI at 50.0 as output declined and new orders fell at the fastest pace in five months. Rising input costs and supply disruptions added pressure, while confidence weakened amid ongoing uncertainty.

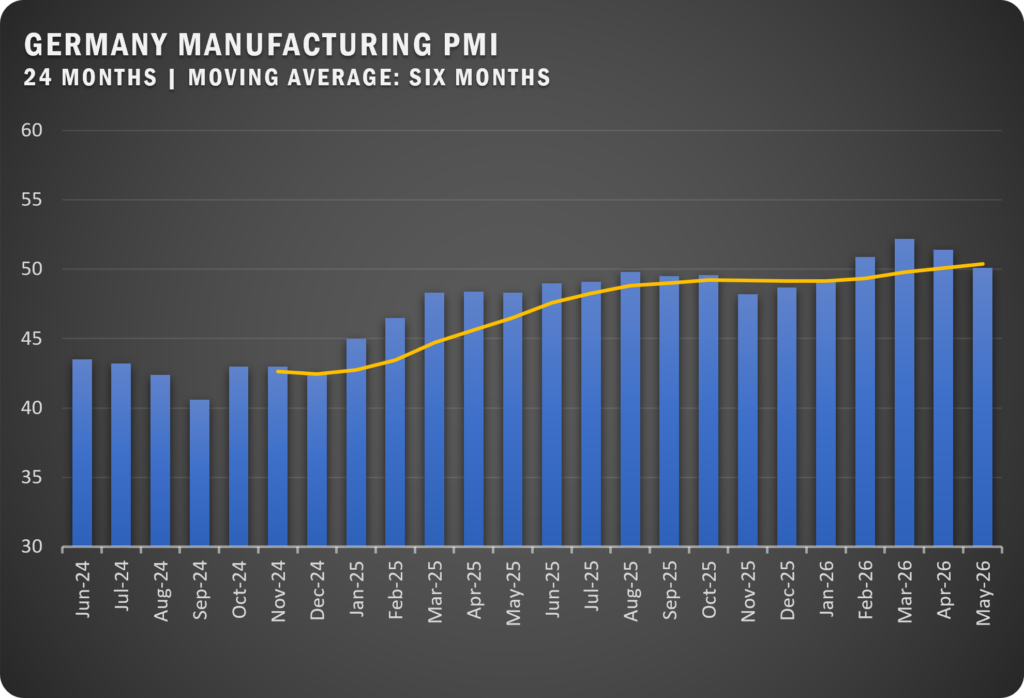

GERMANY: Germany’s manufacturing sector strengthened in March, with the PMI rising to 52.2—its strongest growth in nearly three years—driven by gains in output and new orders. However, supply chain disruptions and surging input costs weighed on sentiment, pushing business confidence down to a four-month low.

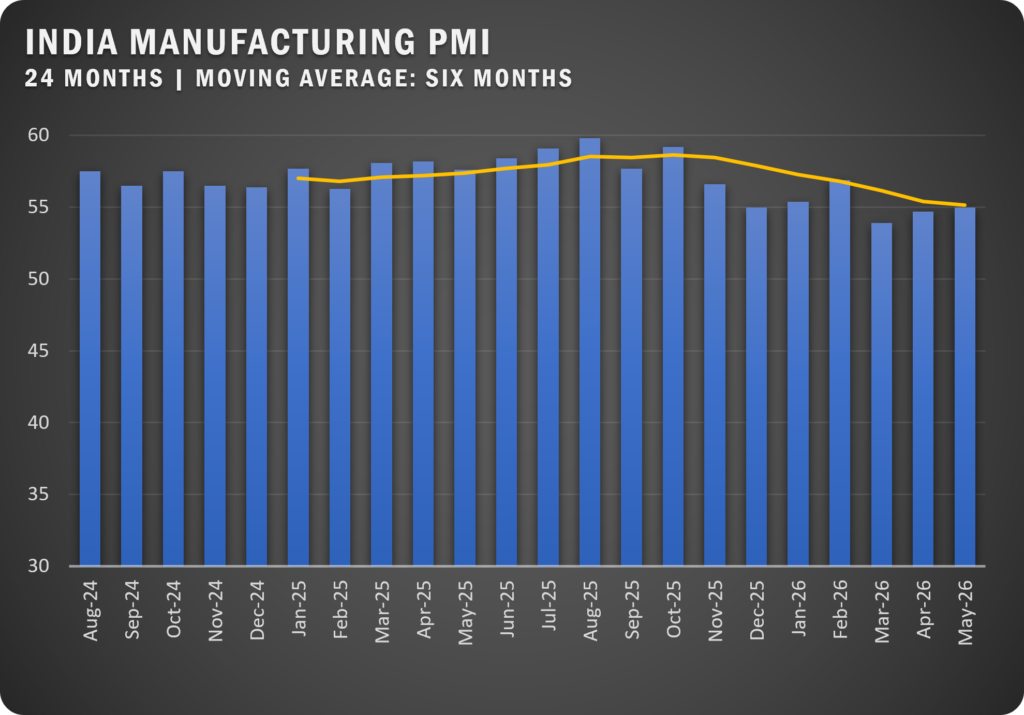

INDIA: India’s manufacturing growth slowed to a near four-year low in March, with the PMI at 53.9 as output and orders expanded more modestly. Despite rising cost pressures, firms increased hiring and maintained optimism, supported by stronger export demand and continued investment.

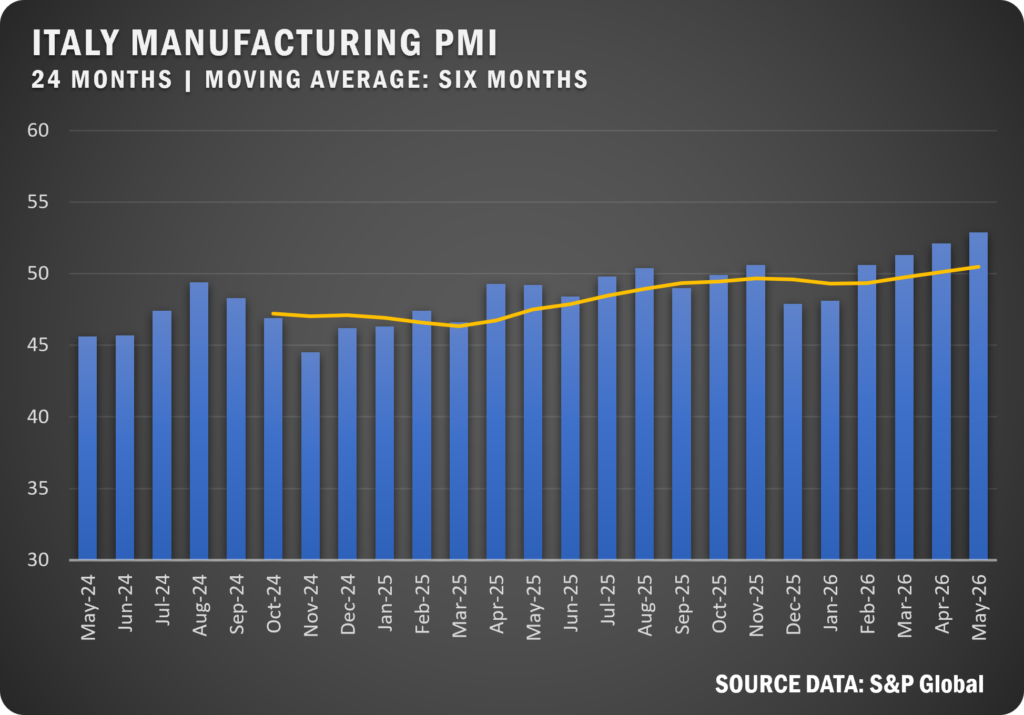

ITALY: Italy’s manufacturing sector posted its strongest performance in over three years in March, with the PMI rising to 51.3 as output, orders, and employment improved. However, supply chain delays and rising costs tied to geopolitical tensions continued to challenge operations, even as confidence remained positive.

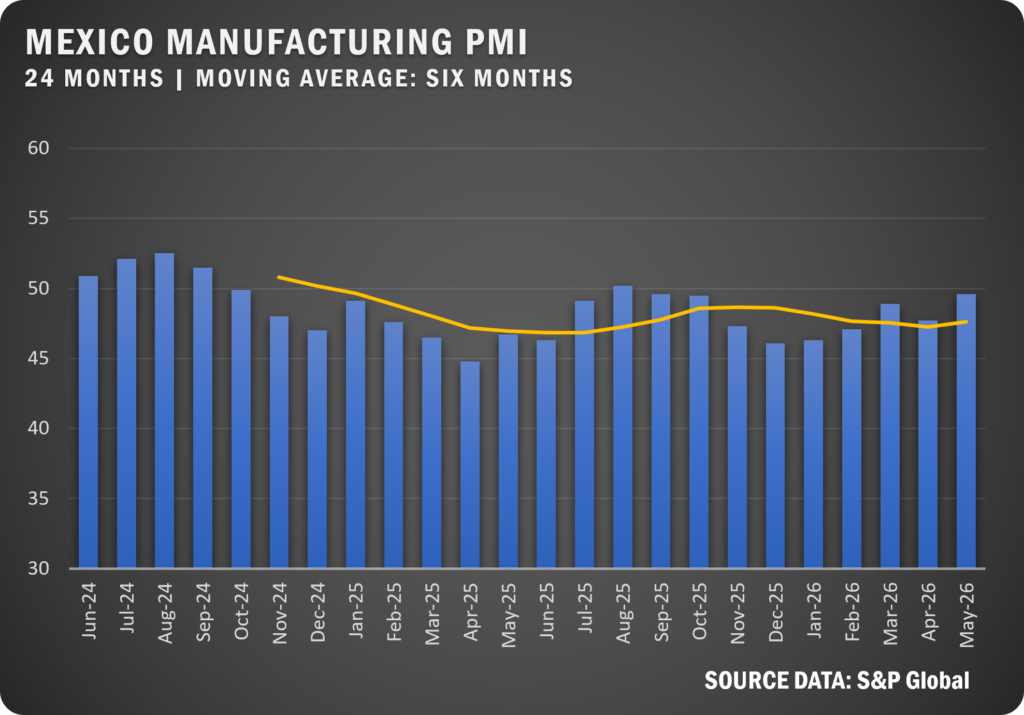

MEXICO: Mexico’s manufacturing contraction eased in March, with the PMI rising to 48.9 as declines in output and new orders moderated. Cost pressures intensified and employment fell, while ongoing tariffs and supply disruptions continued to weigh on demand and operations.

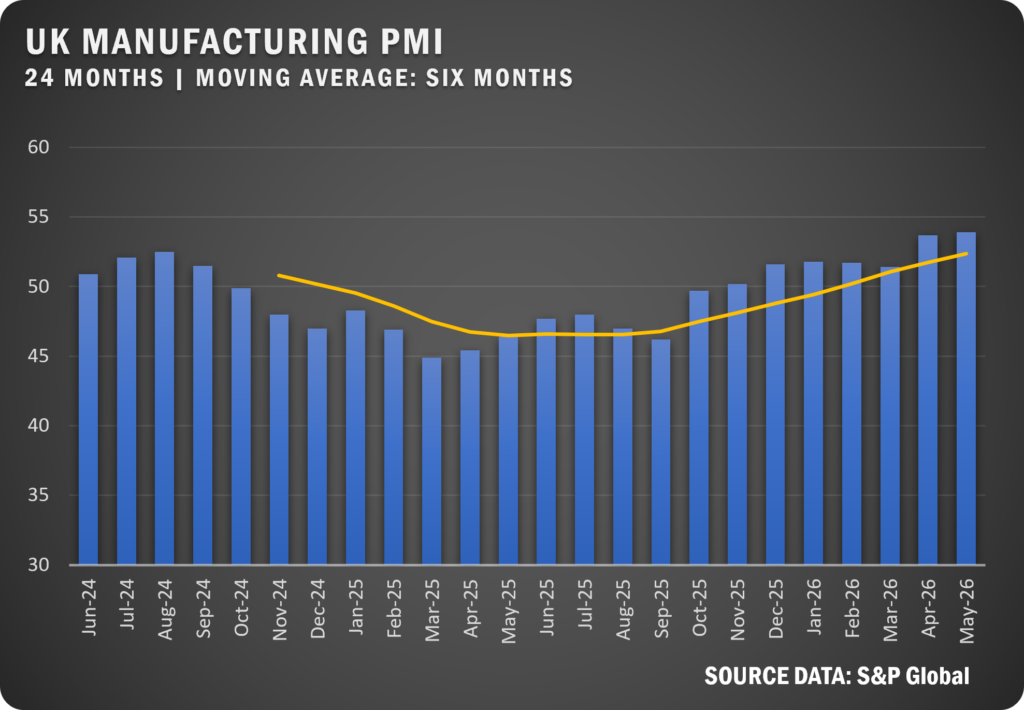

UNITED KINGDOM: UK manufacturing growth remained positive in March, with the PMI at 51.0, though output declined for the first time in six months amid rising uncertainty. Input costs surged due to higher energy prices, prompting firms to raise selling prices while confidence weakened.

Source: Institute for Supply Management®, PMI® (Purchasing Manager Index), Report On Business®. For more information, visit the ISM® website at www.ismworld.org.