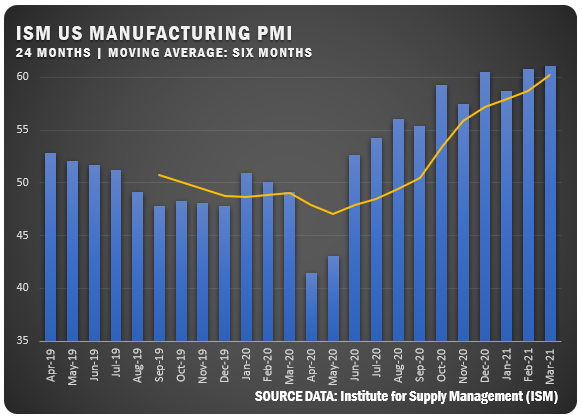

US Manufacturing PMI Jumps 3.9 Percent

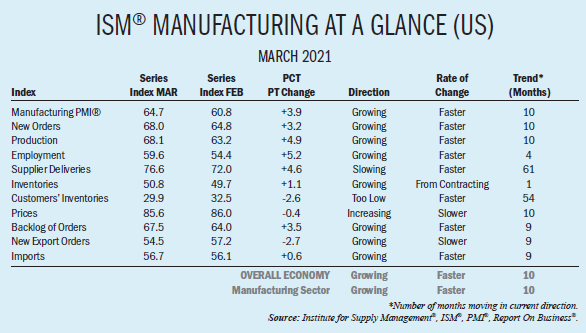

The ISM® Report On Business® for U.S. manufacturing in March showed a big gain with a PMI reading of 64.7 percent, an increase of 3.9 percentage points from the February reading of 60.8 percent. “Manufacturing performed well for the 10th straight month, with demand, consumption and inputs registering strong growth compared to February,” says Timothy R. Fiore, ISM® Manufacturing Business Survey Committee Chair. “Labor-market difficulties at panelists’ companies and their suppliers persist. End-user lead times (for refilling customers’ inventories) are extending due to very high demand and output restrictions as supply chains continue to recover from COVID-19 impacts.”

See the Global PMI Report for March.

ISM® Report Comments (U.S.)

- “The spring and summer months look great for the national oil markets.” (Petroleum and Coal Products)

- “A lack of qualified machine and fabrication shop talent makes it difficult to keep up with production demands when there is no backup (second string). Qualified new hires are an ongoing challenge. We have had to provide better compensation to keep qualified talent. Raw-material prices are up 50 percent to 60 percent over the last six months, which results in increased prices to our customers and a disincentive to build inventory.” (Fabricated Metal Products)

- “Widespread supply chain issues. Suppliers are struggling to manage demand and capacity in the face of chronic logistics and labor issues. No end in sight.” (Machinery)

- “Tremendous stress on the supply chain since the winter storm in Texas. Chemicals are on allocations or unavailable. Resin is on allocation and unavailable.” (Plastics and Rubber Products)

- “Business is even stronger for us this year through the third quarter, and we expect a very healthy growth of our manufacturing sales.” (Electrical Equipment, Appliances and Components)

- “Demand remains strong. Significant supply impacts on raw materials due to the Texas freeze. All major raw-material and suppliers on force majeure.” (Chemical Products)

- “Business conditions are positive for our industry and company. The constraints are mainly related to parts availability (imports, supply chain congestion). Manpower is also a constraint; hiring new members is a challenge.” (Transportation Equipment)

- “Late-winter storms in unexpected [areas] of the U.S. had our organization exercising business-continuity plans on a much more aggressive scale than anticipated. While the storms slowed our supply chain down, we did what we could to meet orders, even though few were short. We feel that in the coming month, we will be able to make up the misses as well as continue strong deliveries in the next month. As consumer confidence grows and the academia market reopens globally, we do expect orders to increase.” (Computer and Electronic Products)

- “Winter Storm Uri has made daily life in-supply chain quite a challenge. Everything from plastic substrates to adhesives have been significantly impacted by the production interruptions.” (Food, Beverage and Tobacco Products)

- “Business bottomed out in February; we are expecting steady improvement through the end of the year. Inflation and material availability, along with logistics, are major concerns.” (Furniture and Related Products)

U.S. SECTOR REPORT

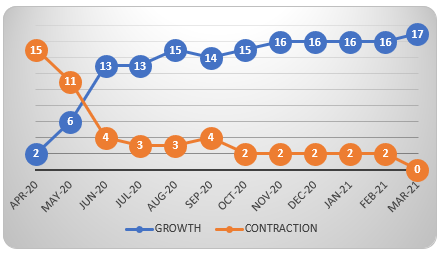

ISM GROWTH SECTORS (17): Textile Mills; Electrical Equipment, Appliances and Components; Machinery; Computer and Electronic Products; Apparel, Leather and Allied Products; Furniture and Related Products; Fabricated Metal Products; Food, Beverage and Tobacco Products; Primary Metals; Plastics and Rubber Products; Paper Products; Transportation Equipment; Chemical Products; Nonmetallic Mineral Products; Miscellaneous Manufacturing; Printing and Related Support Activities; and Petroleum and Coal Products.

ISM CONTRACTION SECTORS (0): No industries reported contraction in March.

Sources: Institute for Supply Management®, ISM®, PMI®, Report On Business®. For more information, visit the ISM® website at www.ismworld.org.